24 September 2015

2015- n° 232207 In September 2015, the economic climate remains low in the building construction

industry Monthly survey of building - September 2015

24 September 2015

2015- n° 232207 In September 2015, the economic climate remains low in the building construction

industry Monthly survey of building - September 2015

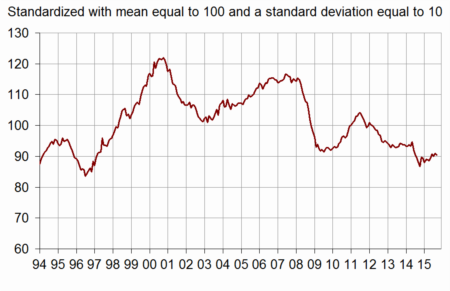

According to the business managers surveyed in September 2015, the business climate is virtually stable in the building construction industry. The composite indicator which measures it has decreased by one point and remains significantly below (90) its long-term average (100). The turning point indicator remains in the favorable zone.

According to the business managers surveyed in September 2015, the business climate is virtually stable in the building construction industry. The composite indicator which measures it has decreased by one point and remains significantly below (90) its long-term average (100). The turning point indicator remains in the favorable zone.

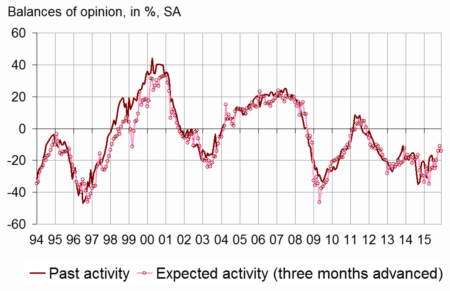

Business managers consider their activity still deteriorated

In September 2015, slightly more business managers than in the previous month have declared a fall in their activity in the recent period and for the next three months. The corresponding balances of opinion are far below their long-term average.

graphiqueActivity – Activity tendency in building construction

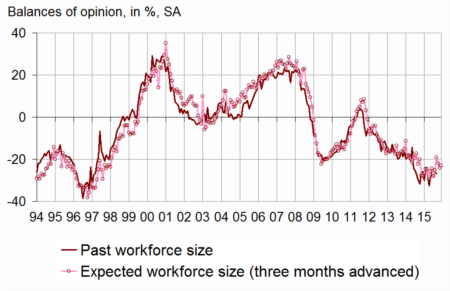

Persistent pessimism about employment

In September 2015, almost as many business managers as in August have indicated a fall in their staff size in the recent period and for the next few months. The corresponding balances remain substantially below their long-term average.

graphiqueWorkforce – Workforce size tendency in building construction

graphiqueClimate – Business climate composite indicator

graphiqueTurningPoint – Turning-point indicator

- Lecture: close to 1 (respectively -1), it indicates a favorable climate (respectively unfavorable).

tableauTableau1 – Building industry economic outlook

| Mean* | June 15 | July 15 | Aug. 15 | Sept. 15 | |

|---|---|---|---|---|---|

| Composite indicator | 100 | 91 | 90 | 91 | 90 |

| Past activity | –4 | –17 | –24 | –22 | –24 |

| Expected activity | –7 | –20 | –14 | –11 | –14 |

| Gen. business outlook | –19 | –27 | |||

| Past employment | –5 | –24 | –28 | –26 | –27 |

| Expected employment | –4 | –19 | –22 | –24 | –23 |

| Opinion on order books | –23 | –56 | –55 | –53 | –52 |

| Order books (in month) | 5,4 | 6,5 | 6,5 | 6,6 | 6,5 |

| Production capacity utilisation rate | 88,6 | 84,5 | 85,0 | 84,7 | 84,3 |

| Obstacles to production increase (in %) | 32 | 22 | 23 | 23 | 22 |

| - Because of workforce shortage (in %) | 14,6 | 2,7 | 3,4 | 2,9 | 2,9 |

| Recruiting problems (in %) | 58 | 41 | |||

| Expected prices | –14 | –32 | –32 | –29 | –30 |

| Cash-flow position | –10 | –21 | |||

| Repayment period | 29 | 43 |

- * Mean since September 1993.

- Source: INSEE, French business survey in the building industry

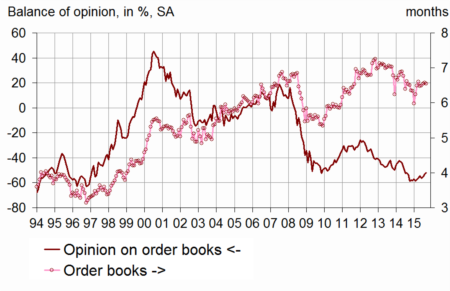

Order books have been considered very low

Business managers’ opinion about their order books remains deteriorated. The corresponding balance has been very low for almost a year now. However, the number of months covered by these order books is practically stable (6.5 months), above its long term average (5.4 months).

graphiqueOrderBooks – Order books

Production capacity has been even less used

Since 2008, the production capacity utilisation rate has been below its long-term average. In September 2015, it has decreased again (from 84.7% to 84.3%). Almost one business manager out of five has reported difficulties in increasing output, against one out of three in average since 1993.

graphiquePcur – Production capacity utilisation rate

Prices has been reported down

In September 2015, almost as many business managers as in August have indicated price falls. The corresponding balance remains substantially below its long-term average.

Documentation

Methodology (2016) (pdf,170 Ko)

Pour en savoir plus