25 July 2017

2017- n° 192In July 2017, the business climate remains very favourable in retail trade and in

trade and repair of motor vehicles Monthly survey of retailing - July 2017

25 July 2017

2017- n° 192In July 2017, the business climate remains very favourable in retail trade and in

trade and repair of motor vehicles Monthly survey of retailing - July 2017

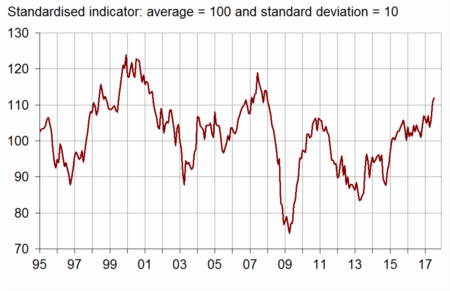

According to the managers in retail trade and in trade and repair of motor vehicles, the business climate remains very favourable in July 2017. The composite indicator that measures it has gained one point compared to June and stands at 112, its highest level since the end of 2007. It has stayed above its long-term average (100) or equal to it since February 2015.

Warning: the seasonal components have been updated in July 2017, as well as the parameters of the three composite indicators, which leads to slight revisions. They are updated once a year.

According to the managers in retail trade and in trade and repair of motor vehicles, the business climate remains very favourable in July 2017. The composite indicator that measures it has gained one point compared to June and stands at 112, its highest level since the end of 2007. It has stayed above its long-term average (100) or equal to it since February 2015.

graphiqueChart_1 – Business climate synthetic indicator

Past and expected activity deemed on the rise

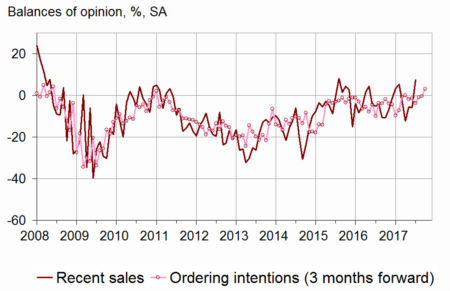

Significantly more managers than in June have declared a rise in their recent sales, the corresponding balance standing at a high level from now on. Anticipations are still optimistic: each of the balances concerning expected sales, ordering intentions and general business outlook remains significantly above its average, reaching its highest point since the beginning of 2008 for the orders, since the mid of 2007 for the general outlook.

Practically as many traders as on the last interrogation have indicated rises in prices on the last as on the next few months; these two balances stand slightly above their average.

The cash position is still estimated rather easy.

tableauTable_1 – Tendency in retail trade and in trade and repair of motor vehicles

| Ave. (1) | April 17 | May 17 | June 17 | July 17 | |

|---|---|---|---|---|---|

| Business climate | 100 | 104 | 106 | 111 | 112 |

| General business outlook | –29 | –17 | –15 | –4 | –2 |

| Recent sales | –7 | –12 | –6 | –6 | 7 |

| Expected sales | –2 | 5 | 2 | 8 | 7 |

| Ordering intentions | –8 | –4 | –1 | 0 | 3 |

| Stocks | 11 | 15 | 10 | 11 | 9 |

| Past selling prices (2) | –6 | –5 | –4 | ||

| Expected selling prices | –3 | –3 | –9 | –3 | –2 |

| Cash position (2) | –15 | –13 | –13 | ||

| Workforce size: recent trend | 1 | 0 | 0 | 2 | 0 |

| Workforce size: future trend | –3 | –5 | –3 | 0 | –2 |

- (1) Average since 1991 (2004 for recent and expected sales and ordering intentions).

- (2) Bi-monthly question (odd-numbered months).

- Source: INSEE - monthly survey in retail trade and in trade and repair of motor vehicles

graphiqueChart_2 – Recent sales and ordering intentions

Balances concerning employment near average

The balances of opinion concerning employment, past as well as expected, have slightly fell back. They remain close to their mean level. In retail trade, however, they returned below their average. In motor car trade and repair, the balance about expected employment is practically stable at a very high level.

In retail trade, the business climate remains favourable

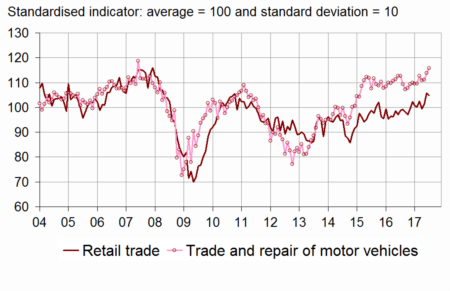

In retail trade, the business climate remains favourable: the composite indicator that measures it, even if it has lost one point, at 105, stays above its average (100).

In non-specialised retail trade, the balance concerning recent sales has significantly increased and has reached its highest point since the beginning of 2008. In specialised trade, this balance has gone on rising but still stands below its mean level.

In retail trade as a whole, the balance concerning expected sales has clearly exceeded its average. Those on ordering intentions and general outlook have barely changed but stand substantially above their average.

The balances about prices have slightly increased, whether on the past or on the future.

The cash flow situation has been estimated slightly more easy than in May, the balance going above its standard level, and at its highest point since the end of 2010.

In trade and repair of motor vehicles, the business climate has reached his highest point since 2007

In trade and repair of motor vehicles and motor cycles, the business climate indicator has gained two points and has reached 116, its highest level for ten years, significantly above its average (100).

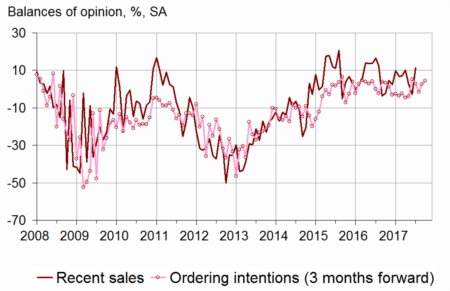

The balance concerning recent sales has recovered. The one about general outlook has gone on increasing. Those on expected sales and ordering intentions have been roughly stable. Each of the four stand significantly above its mean level.

The balance concerning past prices has decreased, the one about expected prices is stable.

The cash situation has been estimated very easy.

graphiqueChart_3 – Recent sales and ordering intentions in trade and repair of motor vehicles

graphiqueChart_4 – Business climate synthetic indicator in retail trade and in trade and repair of motor vehicles

tableauTable_2 – Detailed data

| Ave. (1) | April 17 | May 17 | June 17 | July 17 | |

|---|---|---|---|---|---|

| Retail trade - Global data | |||||

| Business climate | 100 | 99 | 101 | 106 | 105 |

| Gener. busin. outlook | –30 | –19 | –17 | –5 | –3 |

| Recent sales | –6 | –21 | –9 | –7 | 6 |

| Expected sales | 0 | 4 | 5 | 6 | 9 |

| Ordering intentions | –7 | –6 | 0 | –2 | 0 |

| Stocks | 10 | 13 | 6 | 7 | 6 |

| Past selling prices (2) | –8 | –8 | –4 | ||

| Expected selling prices | –5 | –5 | –12 | –5 | –3 |

| Cash position (2) | –13 | –14 | –12 | ||

| Workforce size: recent trend | 2 | 1 | 1 | 2 | 0 |

| Workforce size: future trend | –2 | –5 | –4 | –1 | –4 |

| Non-specialised retail trade | |||||

| Recent sales | –1 | –20 | 5 | 5 | 25 |

| Expected sales | 6 | 14 | 15 | 12 | 21 |

| Ordering intentions | 1 | 3 | 11 | 7 | 13 |

| Stocks | 7 | 16 | 8 | 7 | 2 |

| Past selling prices (2) | –9 | –8 | –3 | ||

| Expected selling prices | –5 | –1 | –13 | –1 | –1 |

| Cash position (2) | –7 | –7 | –7 | ||

| Specialised retail trade | |||||

| Recent sales | –12 | –24 | –25 | –21 | –18 |

| Expected sales | –8 | –10 | –9 | –2 | –7 |

| Ordering intentions | –17 | –19 | –17 | –13 | –16 |

| Stocks | 13 | 9 | 5 | 9 | 8 |

| Past selling prices (2) | –8 | –8 | –4 | ||

| Expected selling prices | –5 | –9 | –11 | –10 | –5 |

| Cash position (2) | –23 | –21 | –17 | ||

| Trade and repair of motor cars and motorcycles | |||||

| Business climate | 100 | 111 | 111 | 114 | 116 |

| Gener. busin. outlook | –28 | –11 | –8 | –3 | 0 |

| Recent sales | –8 | 10 | 2 | –3 | 11 |

| Expected sales | –7 | 4 | –5 | 7 | 5 |

| Ordering intentions | –11 | 3 | –1 | 3 | 4 |

| Stocks | 15 | 21 | 19 | 20 | 20 |

| Past selling prices (2) | 1 | 3 | –4 | ||

| Expected selling prices | 4 | –1 | 2 | 2 | 2 |

| Cash position (2) | –24 | –13 | –14 | ||

| Workforce size: recent trend | –9 | –3 | 0 | 5 | 1 |

| Workforce size: future trend | –7 | 0 | 3 | 6 | 5 |

- (1) Average since 1991 (2003 for trade and repair of motor vehicles and 2004 for recent and expected sales and ordering intentions).

- (2) Bi-monthly question (odd-numbered months).

- Source: INSEE - monthly survey in retail trade and in trade and repair of motor vehicles

Documentation

Methodology (pdf,129 Ko)

Pour en savoir plus