25 September 2012

2012- n° 233The economic climate stays deteriorated in the building industry in September 2012 Monthly survey of building - September 2012

25 September 2012

2012- n° 233The economic climate stays deteriorated in the building industry in September 2012 Monthly survey of building - September 2012

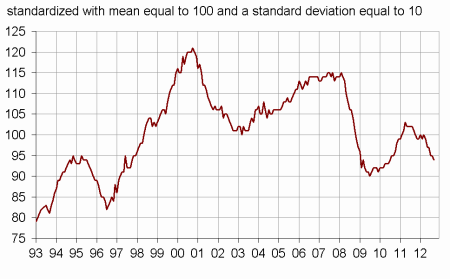

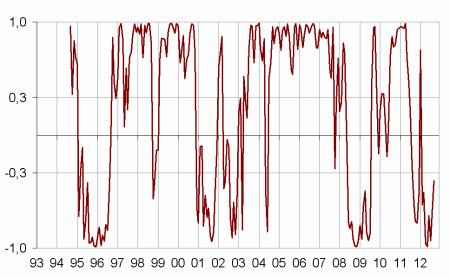

According to the business leaders surveyed in September 2012, the situation is deteriorated in the building industry: the synthetic indicator of business climate loses one point in September, and remains below its long-term average. The turning-point indicator is again in the unfavorable zone.

According to the business leaders surveyed in September 2012, the situation is deteriorated in the building industry: the synthetic indicator of business climate loses one point in September, and remains below its long-term average. The turning-point indicator is again in the unfavorable zone.

graphiqueClimate – Business climate synthetic indicator

graphiqueTurningPoint – Turning-point indicator

- Lecture : close to 1 (respectively -1), it indicates a favorable climate (respectively unfavorable).

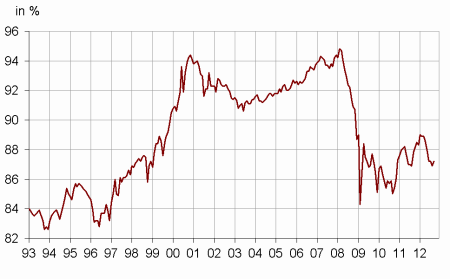

graphiquePcur – Productive capacity utilisation rate

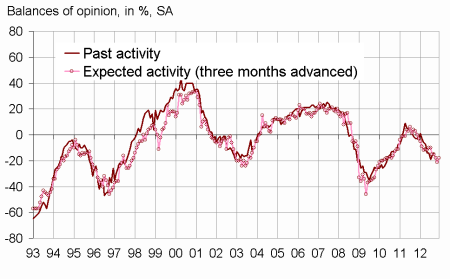

graphiqueActivity – Activity tendency in the building industry

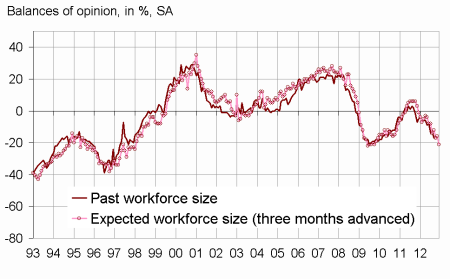

graphiqueWorkforce – Workforce size tendency in the building industry

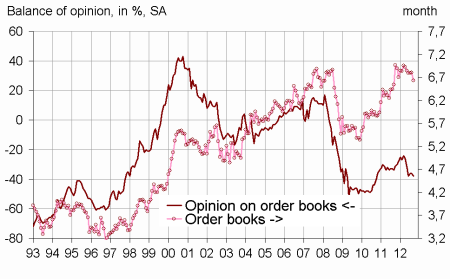

graphiqueOrderBooks – Order books

tableauTableau1 – Building industry economic outlook

Balances of opinion, in %, SA

| Mean* | Jun. 12 | July. 12 | Aug. 12 | Sept. 12 | |

|---|---|---|---|---|---|

| Business climate | 100 | 97 | 95 | 95 | 94 |

| Past activity | –1 | –14 | –19 | –16 | –14 |

| Expected activity | –4 | –15 | –18 | –21 | –18 |

| Gen. business outlook | –16 | –44 | |||

| Past employment | –2 | –8 | –14 | –12 | –17 |

| Expected employment | –2 | –12 | –17 | –16 | –21 |

| Opinion on order books | –19 | –38 | –36 | –36 | –38 |

| Order books (in month) | 5,2 | 6,8 | 6,8 | 6,8 | 6,6 |

| Productive capacity utilisation rate | 89,1 | 87,2 | 87,2 | 86,9 | 87,2 |

| Obstacles to production increase (in %) | 34 | 23 | 26 | 24 | 24 |

| - Because of workforce shortage(in %)** | 16,3 | 7,3 | 6,4 | 5,9 | 5,8 |

| Hiring problems (in %) | 60 | 55 | |||

| Expected prices | –11 | –25 | –33 | –36 | –35 |

| Cash-flow position | –8 | –26 | |||

| Repayment period | 27 | 41 |

- * Mean since september 1993.

- ** This figure refers to all companies that responded to the survey.

Documentation

Methodology (2016) (pdf,170 Ko)

Pour en savoir plus

: bureau-de-presse@insee.fr