25 July 2017

2017- n° 194In July 2017, the business climate improves significantly in wholesale trade Bi-monthly survey of wholesaling - July 2017

25 July 2017

2017- n° 194In July 2017, the business climate improves significantly in wholesale trade Bi-monthly survey of wholesaling - July 2017

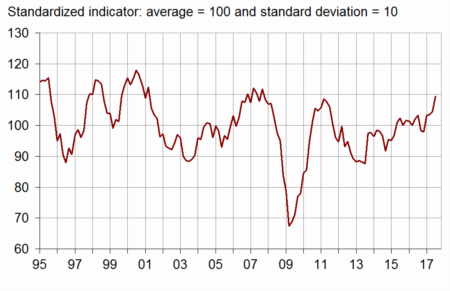

According to the managers surveyed in July 2017, the business climate has strongly improved in the wholesale trade sector. The composite indicator that measures it has gained four points compared to May 2017, and has reached 109, its highest level since the end of 2007, significantly above its long-term average (100).

- Past activity estimated dynamic

- Extremely favourable general business outlook

- Employment prospects remains optimistic

- Statu quo on price falls

- Raw agricultural products and live animals

- Food products and beverages

- Household goods

- Capital goods in information and communication

- Other industrial capital goods

- Other specialised wholesale trade

According to the managers surveyed in July 2017, the business climate has strongly improved in the wholesale trade sector. The composite indicator that measures it has gained four points compared to May 2017, and has reached 109, its highest level since the end of 2007, significantly above its long-term average (100).

graphiqueChart_1 – Composite indicator

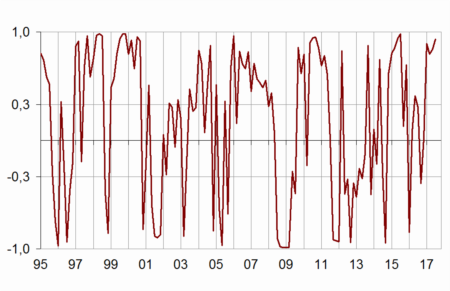

The turning-point indicator has stayed into the area of favourable economic outlook.

graphiqueChart_2 – Turning-point indicator

- Note: close to 1 (respectively −1), this indicator points to a favourable short-term economic situation (respectively unfavourable). Between −0,3 et +0,3: short-term economic uncertainty.

Past activity estimated dynamic

More managers than in May have indicated a rise in their past sales and in their received merchandise, whether in France or abroad. Each of the four balances has progressed from a level already above its average.

Extremely favourable general business outlook

Concerning next months, wholesalers remain optimistic: the balance on total ordering intentions has increased, even if that on ordering from abroad is virtually stable ; the balance on shipments abroad has also gone up. These three balances were already above average. The balance on general business outlook has significantly increased, at its highest point since the beginning of 2001.

Employment prospects remains optimistic

The balance of opinion concerning past workforce has been practically stable since the beginning of the year, above its average. The one about expected workforce remains much higher than its mean level.

Statu quo on price falls

Practically as many wholesalers as in May have declared price falls, whether on the last or on the next few months. Both balances remain below their average.

tableauTable_1 – Total wholesale trade

| Ave.* | Jan. 17 | Mar. 17 | May 17 | July 17 | |

|---|---|---|---|---|---|

| Composite indicator | 100 | 103 | 103 | 105 | 109 |

| General outlook | –24 | –4 | –9 | –5 | 14 |

| Sales | –14 | –12 | –15 | –13 | –6 |

| export sales | –15 | –12 | –12 | –9 | –7 |

| Received merchandise | –9 | –9 | –10 | –8 | –3 |

| received from abroad | –10 | –8 | –5 | –6 | –2 |

| Ordering intentions | –15 | –12 | –11 | –9 | –6 |

| ordering from abroad | –15 | –11 | –8 | –7 | –8 |

| Shipments abroad | –15 | –12 | –14 | –11 | –8 |

| Current stock | 8 | 3 | 4 | 2 | 5 |

| Past workforce | –1 | 3 | 2 | 2 | 3 |

| Expected workforce | –3 | 3 | 4 | 6 | 6 |

| Cash position | –10 | –5 | –5 | –3 | –4 |

| Past selling prices | 7 | 7 | 0 | 0 | –1 |

| Expecting selling prices | 15 | 10 | 6 | 4 | 4 |

- * : average since September 1979

- Source: INSEE - business tendency survey in wholesale trade

Raw agricultural products and live animals

In this sector, the balance concerning past activity remains very low. Those on activity abroad are roughly stable and stay close to their mean level. The balance about ordering intentions has progressed since the beginning of the year but remains below its average.

Food products and beverages

More wholesalers of the food sector than in May have declared a rise in their past activity, in France and abroad. They remain determined about their ordering intentions. The four balances stay above their average, the one about past sales is higher than it has been since the beginning of 2011.

Household goods

Fewer wholesalers than in May have indicated a decrease in their past sales, exports, imports and ordering intentions. The first of these four balances remains below its average, the three others stand above.

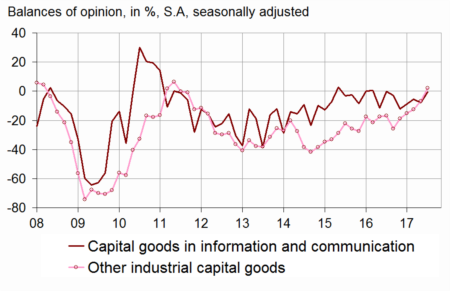

Capital goods in information and communication

In this sector, the balance on past sales has progressed from its mean level; however the one on past exports stays very low. The balances concerning merchandise received from abroad and ordering intentions have fell back but remain above their average.

Other industrial capital goods

In the other industrial goods sector, the balances concerning past sales, imports and ordering intentions have risen, higher than they have been since the mid of 2011 for the two first, the mid of 2008 for the third. The balance on exports is stable, much higher than its average.

Other specialised wholesale trade

In this sector, more traders than in May have indicated an increase in their past activity, in France as well as destined to abroad, and in their ordering intentions. They are as many concerning a rise in imports. Each of the four balances stands significantly above its mean level.

graphiqueChart_3 – Past activity (sales) in capital goods

tableauTable_2 – Wholesale trade sectors

| Ave. * | Jan. 17 | Mar. 17 | May 17 | July 17 | |

|---|---|---|---|---|---|

| Raw agricultural products and live animals | |||||

| Sales | –12 | –37 | –36 | –30 | –30 |

| Export sales | –16 | –29 | –40 | –15 | –16 |

| Merchandise received from abroad | –9 | –15 | –7 | –8 | –10 |

| Ordering intentions | –12 | –45 | –28 | –23 | –20 |

| Current stock | 5 | –11 | –22 | –22 | –8 |

| Food products and beverages | |||||

| Sales | –14 | –17 | –12 | –5 | 0 |

| Export sales | –12 | –6 | –3 | –9 | –4 |

| Merchandise received from abroad | –13 | –17 | –12 | –12 | –3 |

| Ordering intentions | –11 | –7 | –7 | –3 | –2 |

| Current stock | 5 | –6 | 5 | 1 | 4 |

| Household goods | |||||

| Sales | –10 | 1 | –16 | –19 | –14 |

| Export sales | –11 | –13 | 0 | –7 | 0 |

| Merchandise received from abroad | –6 | –4 | 0 | –6 | –2 |

| Ordering intentions | –14 | –8 | –9 | –10 | –5 |

| Current stock | 12 | 5 | 6 | 5 | 4 |

| Capital goods in information and communication | |||||

| Sales | –9 | –9 | –6 | –8 | –1 |

| Export sales | –13 | 7 | –22 | –36 | –39 |

| Merchandise received from abroad | –7 | 1 | 8 | 5 | –3 |

| Ordering intentions | –10 | –4 | –1 | 0 | –5 |

| Current stock | 8 | 8 | 6 | 8 | 5 |

| Other industrial capital goods | |||||

| Sales | –16 | –15 | –12 | –7 | 2 |

| Export sales | –21 | –19 | –13 | –6 | –6 |

| Merchandise received from abroad | –11 | –7 | –3 | –7 | 8 |

| Ordering intentions | –22 | –10 | –14 | –11 | –6 |

| Current stock | 11 | 11 | 9 | 7 | 10 |

| Other specialized wholesale trade | |||||

| Sales | –18 | –4 | –14 | –10 | –2 |

| Export sales | –19 | –7 | –17 | –8 | –4 |

| Merchandise received from abroad | –13 | –3 | –11 | –4 | –4 |

| Ordering intentions | –19 | –6 | –8 | –10 | –3 |

| Current stock | 6 | 7 | 8 | 8 | 12 |

- * : average since September 1979

- Source: INSEE - business tendency survey in wholesale trade

Pour en savoir plus

Time series : Wholesale trade