23 March 2017

2017- n° 75In March 2017, the business climate in manufacturing falls back but remains above

normal Monthly business survey (goods-producing industries) - March 2017

23 March 2017

2017- n° 75In March 2017, the business climate in manufacturing falls back but remains above

normal Monthly business survey (goods-producing industries) - March 2017

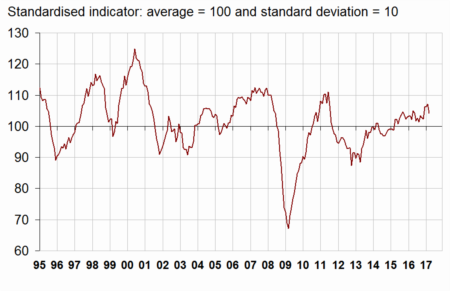

According to the business managers surveyed in March 2017, the business climate in industry has decreased by 3 points after having reached in February its highest level since June 2011. However, at 104, it stands above its long-term average (100).

- Industrialists' opinion about their past activity keeps declining

- In the manufacture of food products and beverages, the business climate is less favourable

- In the manufacture of machinery and equipment goods, the business climate remains well above normal

- The business climate stands above normal in the manufacture of transport equipment

- In “other manufacturing”, the business climate declines after reaching its highest level since June 2011

According to the business managers surveyed in March 2017, the business climate in industry has decreased by 3 points after having reached in February its highest level since June 2011. However, at 104, it stands above its long-term average (100).

graphiqueGraph 1 – Business climate in industry - Composite indicator

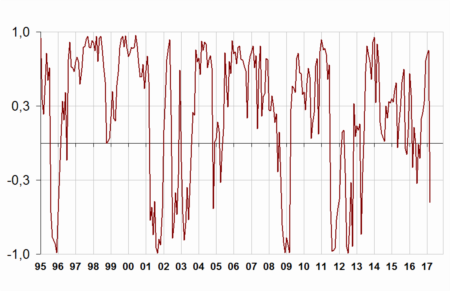

The turning-point indicator is in the zone indicating an unfavourable economic outlook.

graphiqueGraph 2 – Turning-point indicator

- How to read it: close to 1 (respectively -1), the indicator points to a favourable short-term economic situation (respectively unfavourable). Between -0.3 and +0.3: uncertainty area.

Industrialists' opinion about their past activity keeps declining

In March 2017, the balance of industrialist's opinion on their past activity has dropped again and is now slightly below normal. The balance on personal production expectations has fallen back after having reached in February its highest level since January 2008. It has returned to a level close to that of January, still well above its mean.

Business managers are a little less upbeat on general production prospects for the sector. The corresponding balance has slightly decreased but remains significantly above its long-term average, that it has exceeded since February 2015.

In March, global and export order books have slightly thinned albeit remaining significantly above normal.

Finally, almost as industrialists as in February consider that finished-goods inventories are below normal: the corresponding balance is virtually stable below its long-term average.

tableauTable 1 – Industrialists' opinion on manufacturing activity

| Manufacturing industry | Ave.* | Dec. 16 | Jan. 17 | Feb. 17 | March 17 |

|---|---|---|---|---|---|

| Composite indicator | 100 | 106 | 106 | 107 | 104 |

| Past activity | 4 | 19 | 12 | 8 | 2 |

| Finished-goods inventory | 13 | 8 | 6 | 6 | 7 |

| Global order books | –18 | –10 | –10 | –8 | –10 |

| Export order books | –14 | –9 | –4 | –3 | –5 |

| Personal production expectations | 5 | 8 | 13 | 19 | 12 |

| General production expectations | –9 | 6 | 7 | 5 | 3 |

- * Long-term average since 1976.

- Source: INSEE - Monthly business tendency survey in industry

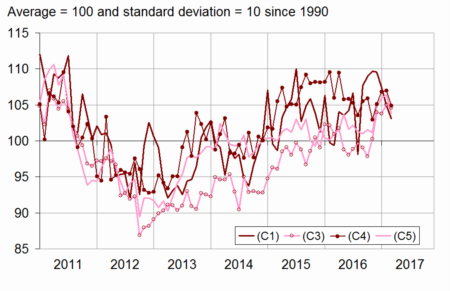

The downturn in the business climate in industry has arisen from a decline in all sub-sectors, except in machinery and equipment goods where the business climate is stable.

In the manufacture of food products and beverages, the business climate is less favourable

In the manufacture of food products and beverages, the business climate has decreased by two points in March (at 103) but remains above its long-term average. This further decline mainly stems from a further decrease in the balance of opinion on past activity.

In the manufacture of machinery and equipment goods, the business climate remains well above normal

In the manufacture of machinery and equipment goods, the business climate is stable at 105, above normal. On the one hand, order books have thinned, on the other hand the balance on personal production expectations has kept improving, reaching its highest level since March 2011.

In the computer, electronic and optical product industry, the business climate, already significantly above normal, has recovered. In machinery and equipment, the business climate is virtually stable above normal. However, in electrical equipment, it has slightly fallen back and has returned to its long-term average.

The business climate stands above normal in the manufacture of transport equipment

In the manufacture of transport equipment, the business climate has decreased by two points but stands at 105, above its long-term average. This decline mainly results from the decrease in the balances on global order books, personal production expectations and past activity.

In the manufacture of motor vehicles, trailers and semi-trailers, the business climate has fallen back while it is stable in other transport equipment. Both are above normal.

In “other manufacturing”, the business climate declines after reaching its highest level since June 2011

In overall “other manufacturing”, the business climate has decreased by two points after having reached its highest level since June 2011. However, at 104, it remains above normal. This fall stems from order books, in particular for orders from abroad, as well as from balances on past activity and on personal production expectations.

In clothing-textiles, wood-paper, chemicals and in basic metals, the business climate has diminished albeit remaining above normal. However, it is stable at its highest level since June 2011 in rubber and plastic products and has slightly improved in the “other manufacturing industries”.

graphiqueGraph 3 – Business climates in a sector-based approach

- Legend: (C1): Manufacture of food products and beverages - (C3): Machinery and equipment goods - (C4): Manufacture of transport equipment - (C5): Other manufacturing

tableauTable 2 – Business climates in a sector-based approach

| NA* : (A17) et [A38 et A64] | Weights** (%) | Jan. 17 | Feb. 17 | March 17 |

|---|---|---|---|---|

| (C1) Man. of food products and beverages | 21 | 107 | 105 | 103 |

| (C3) Machinery and equipment goods | 11 | 104 | 105 | 105 |

| [CI] Computer, electronic and optical products | 3 | 110 | 108 | 111 |

| [CJ] Electrical equipment | 3 | 102 | 102 | 100 |

| [CK] Machinery and equipment | 5 | 100 | 104 | 103 |

| (C4) Man. of transport equipment | 15 | 107 | 107 | 105 |

| [CL1] Motor vehicles, trailers and semi-trailers | 7 | 108 | 108 | 105 |

| [CL2] Other transport equipment | 8 | 104 | 104 | 104 |

| (C5) Other manufacturing | 46 | 106 | 106 | 104 |

| [CB] Textiles, clothing industries, leather and footwear industry | 2 | 108 | 109 | 106 |

| [CC] Wood, paper, printing | 5 | 106 | 108 | 104 |

| [CE] Chemicals and chemical products | 9 | 106 | 110 | 105 |

| [CG] Rubber and plastic products | 7 | 106 | 107 | 107 |

| [CH] Basic metals and fabricated metal products | 11 | 105 | 103 | 101 |

| [CM] Other manufacturing industries | 9 | 100 | 100 | 102 |

- * NA: aggregated classification, based on the French classification of activities NAF rév.2.

- ** Weights used to aggregate sub-sector's balances of opinion.

- Source: INSEE - Monthly business tendency survey in industry

Documentation

Methodology (pdf,133 Ko)

Pour en savoir plus

Time series : Industry - Activity and demand