27 January 2017

2017- n° 24In January 2017, the economic climate brightens slightly more in civil engineering Quaterly survey of public works - January 2017

27 January 2017

2017- n° 24In January 2017, the economic climate brightens slightly more in civil engineering Quaterly survey of public works - January 2017

According to the business managers surveyed in January 2017, the economic climate in civil engineering is slightly more favourable than in October 2016.

According to the business managers surveyed in January 2017, the economic climate in civil engineering is slightly more favourable than in October 2016.

Business managers' opinion on their activity has improved again slightly

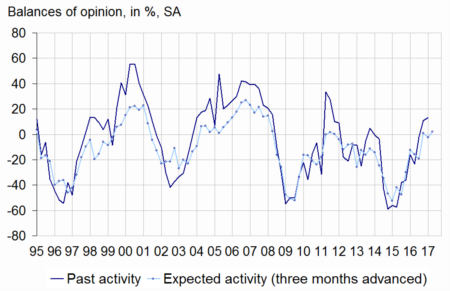

In January 2017, more business managers than in October 2016 report an increase in their past and expected activity. The balances on expected activity have increased for both private-sector and public-sector projects. The balance on past activity for private-sector projects has increased too. However, it is stable for public-sector projects. Those four balances stand above their long term average.

Moreover, the balance on order books has improved again and has outstripped its long term-average, for the first time since early 2014.

Fewer production constraints

Slightly fewer business managers than in October 2016 have felt constraints due to workforce shortage. Obstacles to production remain below normal: 9% of businesses indicate being hampered because of a workforce shortage, against 14% on long-term average.

Employment prospects are still improving

More business managers forecast to increase their workforce. Since April 2016, the balance of opinion on expected workforce has improved steadily. It stands above its long-term average.

tableauTable1 – Public works economic outlook

| Mean* | April 16 | July 16 | Oct. 16 | Jan. 17 | |

|---|---|---|---|---|---|

| Past activity | –7 | –24 | –2 | 11 | 13 |

| - public-sector project | –13 | –36 | –18 | 1 | 1 |

| - private-sector project | –11 | –16 | 4 | 13 | 17 |

| Expected activity | –15 | –19 | 1 | –2 | 2 |

| - public-sector project | –18 | –33 | –6 | –13 | –9 |

| - private-sector project | –17 | –15 | 2 | 4 | 6 |

| Opinion on order books | –27 | –57 | –41 | –32 | –25 |

| Obstacles to production increase because of workforce shortage (in %) | 14 | 4 | 7 | 11 | 9 |

| Expected workforce | –16 | –25 | –7 | 3 | 6 |

- Note: the balances of opinion by costumer may differ from the balance of the whole, because sometimes the firms don't distinguish public-sector project and private-sector project.

- * Mean since January 1981

graphiqueGraph1 – Activity tendency in public works

Pour en savoir plus