25 November 2016

2016- n° 308In November 2016, households' confidence is stable Monthly consumer confidence survey - November 2016

25 November 2016

2016- n° 308In November 2016, households' confidence is stable Monthly consumer confidence survey - November 2016

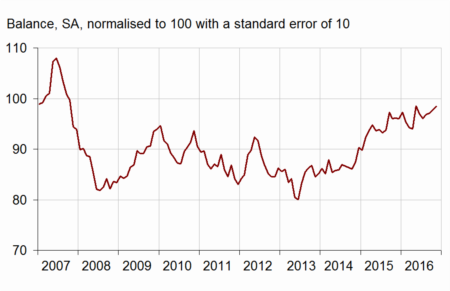

In November 2016, households' confidence is stable: the synthetic confidence index stands at 98. Thus, it remains below its long-term average (100).

In November 2016, households' confidence is stable: the synthetic confidence index stands at 98. Thus, it remains below its long-term average (100).

graphiqueGraph1 – Consumer confidence synthetic index

- Source: INSEE

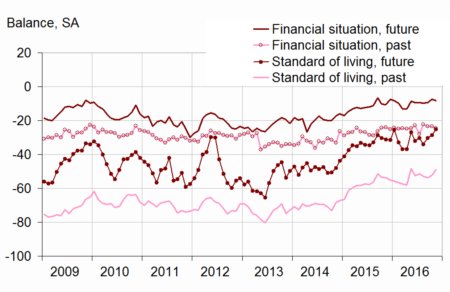

Personal situation

Past financial situation: decreasing slightly

In November, households' opinion of their personal financial situation in the past twelve months has worsened slightly: the corresponding balance has lost 2 points. It has moved further from its long term average anew. Households' opinion of their personal financial situation in the next twelve months has barely changed: the balance has lost 1 point after a gain of 3 points in October and stays slightly below its long-term average.

The share of households considering it has been a suitable time to make major purchases is stable and stands above its long-term average.

Saving capacity: virtually stable

In November, households' balance of opinion on their expected saving capacity is virtually stable (+ 1 point): it thus remains slightly above its long-term average. The balance concerning their current saving capacity holds steady, slightly below its long-term average.

The share of households considering it has been a suitable time to save is stable, clearly below its long-term average.

graphiqueGraph2 – Balances on personal financial situation and standard of living in France

- Source: INSEE

Economic situation in France

Past and future standard of living in France: increasing

In November, household's opinion of the future standard of living in France has kept growing: the corresponding balance has increased for the fifth consecutive month. With a gain of 4 points, it has come back to its long-term average, that is its highest level since January 2016. The balance on the past standard of living has grown by 3 points, and has moved closer to its long-term average.

Unemployment: fears decreasing clearly

After being aroused in October, households' fears about unemployement have lessened clearly in November (−11 points). Thus, the corresponding balance has returned below its long-term average.

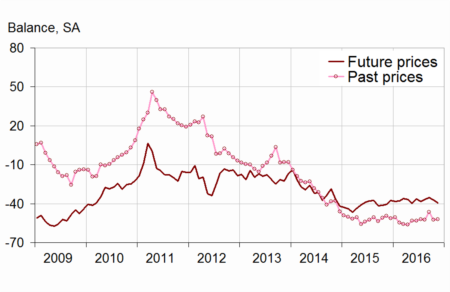

Expected inflation: decreasing

In November, households are a little less numerous to consider that prices are likely to increase during the next twelve months: the corresponding balance has lost 2 points and has continued to drift away from its long-term average. They are almost as numerous as in October to consider that prices fell during the past 12 months: the balance has gained 1 point but remains clearly below its long-term average.

graphiqueGraph3 – Households' unemployment expectations

- Source: INSEE

graphiqueGraph4 – Households' perception of prices

- Source: INSEE

tableauTable – CONSUMER OPINION: synthetic index and opinion balances

| 2016 | |||||

|---|---|---|---|---|---|

| Av. (1) | Aug. | Sept. | Oct. | Nov. | |

| Synthetic index (2) | 100 | 97 | 97 | 98 | 98 |

| Financial sit., past 12 m. | –21 | –22 | –24 | –23 | –25 |

| Financial sit., next 12 m. | –5 | –10 | –10 | –7 | –8 |

| Current saving capacity | 8 | 10 | 9 | 6 | 6 |

| Expected saving capacity | –9 | –9 | –7 | –7 | –6 |

| Savings intentions, next 12 m. | 18 | 0 | 1 | –2 | –2 |

| Major purchases intentions, next 12 m. | –15 | –10 | –6 | –5 | –5 |

| Standard of living, past 12 m. | –45 | –53 | –54 | –52 | –49 |

| Standard of living, next 12 m. | –25 | –34 | –30 | –29 | –25 |

| Unemployment, next 12 m. | 35 | 34 | 30 | 40 | 29 |

| Consumer prices, past 12 m. | –14 | –52 | –47 | –53 | –52 |

| Consumer prices, next 12 m. | –34 | –37 | –35 | –37 | –39 |

- (1) Average value between January 1987 and December 2015

- (2) This indicator is normalised in such a way that its average equals 100 and standard error equals 10 over the estimation period (1987-2015).

- Source: INSEE, monthly consumer confidence survey

Pour en savoir plus