19 June 2012

2012- n° 153In June 2012, the economic climate remains deteriorated in services Monthly survey of services - June 2012

19 June 2012

2012- n° 153In June 2012, the economic climate remains deteriorated in services Monthly survey of services - June 2012

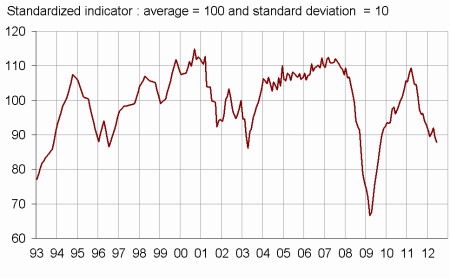

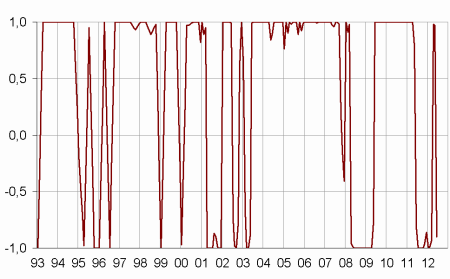

According to the business leaders surveyed in June 2012, the economic situation in services remains dete-riorated. The business climate synthetic indicator drops by one point compared with May and is 88. He remains below its long-term average. The turning point indicator falls and now indicates an unfavourable economic situation.

Warning : seasonal coefficients were updated for this survey.

According to the business leaders surveyed in June 2012, the economic situation in services remains deteriorated. The business climate synthetic indicator drops by one point compared with May and is 88. He remains below its long-term average. The turning point indicator falls and now indicates an unfavourable economic situation.

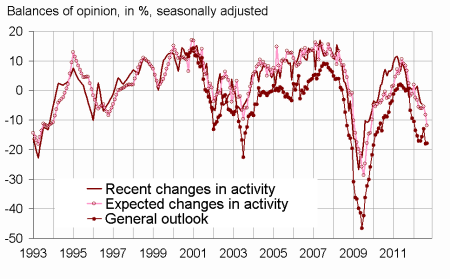

The business leaders consider that their activity decreased during the last few months, and revise downward their expectations of activity for the months to come. The general outlook is unchanged from May but remains below its long-term average.

graphiqueGraph1 – Business climate synthetic indicator

graphiquegraph_retourn – Turning point indicator

- Note: close to 1 (respectively -1), this indicator indicates a favourable short-term economic situation (respectively unfavourable).

graphiqueGraph2 – Activity

tableauTable_quarter – Economic outlook in the services sector

| Average* | Mar. 12 | Apr. 12 | May 12 | June 12 | |

|---|---|---|---|---|---|

| Business climate synthetic indicator | 100 | 90 | 92 | 89 | 88 |

| General outlook | –5 | –16 | –13 | –18 | –18 |

| Past activity | 4 | 2 | –1 | –4 | –5 |

| Expected activity | 4 | –6 | –5 | –8 | –12 |

| Expected demand | 1 | –11 | –6 | –9 | –9 |

| Business situation | 0 | –5 | –8 | –13 | –16 |

| Past selling prices | –2 | –2 | –4 | –4 | –5 |

| Expected selling prices | –1 | –1 | –4 | –6 | –7 |

| Past employment | 4 | 1 | –3 | –2 | –15 |

| except temporary work agencies | 1 | 0 | –4 | 0 | –7 |

| Expected employment | 3 | –3 | –2 | –12 | –10 |

| except temporary work agencies | 0 | –4 | –4 | –7 | –7 |

| Investments | |||||

| Past investments | 2 | 1 | 3 | 0 | 2 |

| Expected investments | 2 | 1 | –1 | –3 | –4 |

- * Average of the balances of opinion since 1988

- Source: Insee

Documentation

Methodology (2016) (pdf,158 Ko)

Pour en savoir plus

Time series : Economic outlook surveys – Services