24 December 2013

2013- n° 298In Q3 2013, GDP (-0.1% after +0.6%) and households’ purchasing power (-0.1% after

+0.5%) slightly decreased Quarterly national accounts - detailed figures - 3rd quarter 2013

24 December 2013

2013- n° 298In Q3 2013, GDP (-0.1% after +0.6%) and households’ purchasing power (-0.1% after

+0.5%) slightly decreased Quarterly national accounts - detailed figures - 3rd quarter 2013

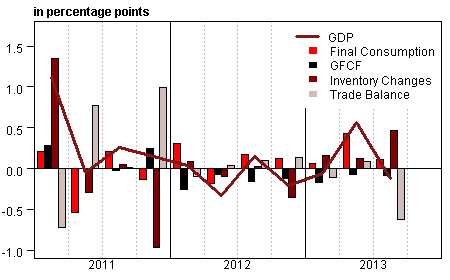

In Q3 2013, GDP in volume terms* was slightly down (–0.1%), after a rebound in Q2 (+0.6%).

In Q3 2013, GDP in volume terms* was slightly down (–0.1%), after a rebound in Q2 (+0.6%).

Household consumption expenditure decelerated (+0.1% after +0.4%). Furthermore, total gross fixed capital formation (GFCF) decreased by 0.4%, as in the previous quarter. Overall, final domestic demand (excluding inventory changes) marked time and had a neutral contribution to GDP after +0.4 point in Q2. Exports fell again (–1.3% after +1.9%) whereas imports remained dynamic (+0.9% after +1.5%). Hence, the foreign trade balance had a negative accounting contribution to GDP growth: –0.6 point, after +0.1 point the previous quarter. Conversely, changes in inventories contributed for +0.5 point to GDP growth (after +0.1 point).

Households’ purchasing power slowed down

Wages earned by households slightly decelerated (+0.3% after +0.5%), mainly due to deceleration of wages paid by non-financial corporations (NFC). Social benefits remained dynamic (+0.7% after +0.8% in previous quarter). In contrast, taxes on income and wealth accelerated again in Q3 (+1.9% after +1.4%) partly as a result of budget consolidation measures passed for 2013: de-indexation of the income tax thresholds, creation of a 45% bracket, lowering of the family quotient ceiling. Overall, in nominal terms, household disposable income slowed down (+0.1% after +0.4%).

graphiqueGraph1 – GDP and its main components

tableauTab1 – Goods and services:supply and uses chain-linked volumes

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | 2013 (ovhg) | |

|---|---|---|---|---|---|---|

| GDP | -0.2 | -0.1 | 0.6 | -0.1 | 0.0 | 0.1 |

| Imports | -1.2 | 0.1 | 1.5 | 0.9 | -0.9 | 0.9 |

| Households' consumption *expenditure | 0.0 | -0.1 | 0.4 | 0.1 | -0.4 | 0.3 |

| General government's *consumption expenditure | 0.4 | 0.4 | 0.7 | 0.2 | 1.4 | 1.6 |

| GFCF | -0.6 | -0.9 | -0.4 | -0.4 | -1.2 | -2.3 |

| *of which Non financial corporated and unincorporated enterprises | -0.4 | -0.8 | 0.1 | -0.4 | -1.9 | -1.9 |

| Households | -1.0 | -1.3 | -1.7 | -0.6 | -0.4 | -3.8 |

| General government | -0.7 | -0.5 | 0.3 | -0.2 | -0.6 | -1.2 |

| Exports | -0.8 | -0.3 | 1.9 | -1.3 | 2.5 | 0.2 |

| Contributions : | ||||||

| Internal demand excluding inventory changes | 0.0 | -0.1 | 0.4 | 0.0 | -0.1 | 0.1 |

| Inventory changes | -0.3 | 0.2 | 0.1 | 0.5 | -0.8 | 0.2 |

| Net foreign trade | 0.1 | -0.1 | 0.1 | -0.6 | 1.0 | -0.2 |

tableauTab2 – Sectoral accounts

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | 2013 (ovhg) | |

|---|---|---|---|---|---|---|

| Profit ratio of NFC* (level) | 28.0 | 28.0 | 28.2 | 27.7 | 28.3 | |

| Household purchasing power | -0.9 | 0.9 | 0.5 | -0.1 | -0.9 | 0.4 |

- *NFC: non-financial corporations

tableauTab3 – GDP and components: prices indices

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | 2013 (ovhg) | |

|---|---|---|---|---|---|---|

| GDP | 0.2 | 0.5 | 0.1 | 0.1 | 1.5 | 1.1 |

| Imports | 0.2 | -0.6 | -0.9 | 0.2 | 1.9 | -0.9 |

| Cons. Exp. : | ||||||

| - Households | 0.2 | 0.3 | -0.1 | 0.2 | 1.9 | 0.6 |

| - GG* | 0.1 | 0.1 | 0.0 | 0.1 | 1.1 | 0.5 |

| Total GFCF | 0.1 | 0.4 | -0.1 | 0.3 | 1.7 | 0.7 |

| - of which Households | -0.1 | 0.3 | -0.3 | 0.5 | 2.3 | 0.3 |

| - of which NFE | 0.1 | 0.6 | 0.0 | 0.3 | 1.3 | 1.0 |

| - of which GG | 0.2 | 0.2 | -0.1 | 0.3 | 2.2 | 0.7 |

| Exports | 0.2 | -0.2 | -0.4 | -0.2 | 1.2 | -0.1 |

- *GG: General Government

tableauTab4 – Manufactured goods: supply and uses in volume

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | 2013 (ovhg) | |

|---|---|---|---|---|---|---|

| Industrie’s production | -2.0 | 0.5 | 2.0 | -1.0 | -2.8 | 0.1 |

| - of which value added | -1.7 | 0.0 | 1.2 | -0.7 | -2.0 | -0.7 |

| Imports | -1.6 | 0.1 | 1.5 | 1.5 | 0.3 | 0.4 |

| Intermediate uses | -1.1 | 0.0 | 1.5 | -0.3 | -1.8 | 0.2 |

| Cons. Exp. : | ||||||

| - of households | -0.2 | -0.7 | 0.4 | 0.4 | -1.2 | -0.4 |

| - of GG | 1.6 | 1.5 | 1.4 | 1.0 | 4.3 | 4.7 |

| Total GFCF | -1.0 | -0.9 | -0.3 | 1.0 | -3.0 | -2.2 |

| - of which NFC | -1.1 | -1.1 | -0.4 | 1.1 | -3.7 | -2.7 |

| - of which GG | -0.1 | 0.0 | 0.2 | 0.2 | 1.0 | -0.1 |

| Exports | -1.7 | -0.5 | 2.8 | -1.9 | 3.0 | -0.1 |

| Inventory changes (contribution) | -0.9 | 1.1 | 0.1 | 0.9 | -2.5 | 0.8 |

tableauTab5 – Households’ disposable income and ratios of households’ account

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | 2013 (ovhg) | |

|---|---|---|---|---|---|---|

| HDI | -0.7 | 1.2 | 0.4 | 0.1 | 0.9 | 1.0 |

| Household purchasing power | -0.9 | 0.9 | 0.5 | -0.1 | -0.9 | 0.4 |

| HDI by cu* (purchasing power) | -1.1 | 0.7 | 0.3 | -0.2 | -1.5 | -0.1 |

| Adjusted HDI (purchasing power) | -0.6 | 0.7 | 0.5 | 0.0 | -0.4 | 0.6 |

| Saving rate (level) | 15.0 | 15.8 | 15.9 | 15.7 | 15.6 | |

| Financial saving rate (level) | 5.7 | 6.6 | 6.9 | 6.7 | 6.2 |

- *cu: consumption unit

tableauTab6 – Ratios of non-financial corporations’ account

| 2012 Q4 | 2013 Q1 | 2013 Q2 | 2013 Q3 | 2012 | |

|---|---|---|---|---|---|

| Profit share | 28.0 | 28.0 | 28.2 | 27.7 | 28.3 |

| Investment ratio | 19.2 | 19.1 | 19.0 | 19.0 | 19.4 |

| Savings ratio | 11.9 | 12.3 | 12.7 | 11.1 | 12.8 |

| Self-financing ratio | 61.8 | 64.4 | 66.9 | 58.5 | 65.9 |

Moreover consumption prices increased this quarter (+0.2% after –0.1% in Q2) therefore households’ purchasing power was slightly down (–0.1%, after +0.5%). Taken individually (measured per consumption unit), it decreased by 0.2% (after +0.3%).

Households’ consumption in value increased by 0.3% (as in previous quarter), faster than nominal income. Therefore the savings ratio stepped back from 15.9% to 15.7% in Q3.

Non financial corporation’s profit share at the lowest since 1985

In Q3 2013, non financial corporation’s value added decelerated sharply (–0.3% in current prices after +0.9%). Wages paid decelerated but still increased (+0.2% after +0.6%): employment decreased at the same rate (–0.2% after –0.1%) and wage per capita slowed down (+0.4% after +0.7%). Furthermore employee contributions and other taxes on production accelerated (+0.9% after +0.6%). Overall, gross operating surplus of non-financial corporations downturned (–2.1% after +1.7%) and their profit margin stepped back to 27.7% in Q3 (–0.5 point from Q2). It is the lowest level since Q4 1985.

GDP decrease is confirmed (–0.1%)

Compared to the previous release, GDP decrease in Q3 is unchanged (–0.1%). However the growth of GDP in Q2 is slightly scaled up from +0.5% to +0.6%. Revisions are due to the integration of data known since then and to the updates of seasonal adjustments. The annual growth rate carried over at Q3 point remains unchanged (+0.1%).

Pour en savoir plus