23 August 2018

2018- n° 217In August 2018, the business climate weakens slightly in the building construction

industry Monthly survey of building - August 2018

23 August 2018

2018- n° 217In August 2018, the business climate weakens slightly in the building construction

industry Monthly survey of building - August 2018

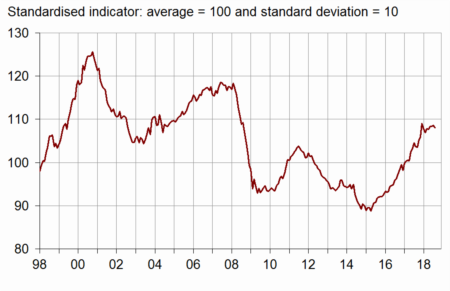

According to the business managers in the building construction industry surveyed in August 2018, the business climate has weakened slightly. The composite indicator has slipped back by one point. Returning to its May-June level (108), it remains however well above the long-term average (100).

Warning: in the publication of August 2018, the seasonal coefficients have been updated as well as the parameters of the composite indicator. As a result, the set of results previously published from this survey is subject to slight revisions.

According to the business managers in the building construction industry surveyed in August 2018, the business climate has weakened slightly. The composite indicator has slipped back by one point. Returning to its May-June level (108), it remains however well above the long-term average (100).

graphiqueGraph1 – Business climate composite indicator

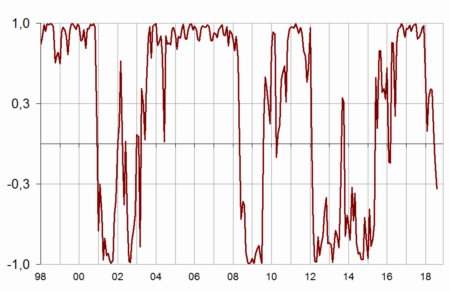

The turning point indicator has gone into the unfavourable outlook area for the first time since June 2015.

graphiqueGraph2 – Turning-point indicator

- Note: close to 1 (respectively –1), it indicates a favourable climate (respectively unfavourable). The uncertainty area is between –0.3 and +0.3

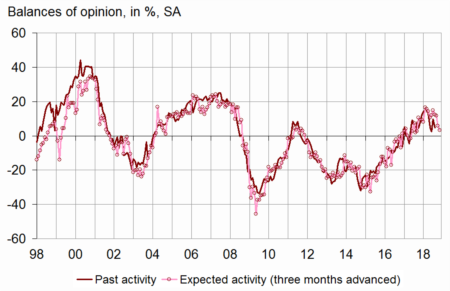

The business managers' opinion on their past and expected activity has deteriorated

In August 2018, significantly fewer business managers than in the previous month have indicated an increase in their activity over the last three months. The corresponding balance has fallen back but remains above its long-term average. Otherwise, the balance of opinion on expected activity has decreased again while also remaining above its long-term average.

graphiqueGraph3 – Activity tendency in building construction

tableauTable1 – Building industry economic outlook

| Mean* | May 18 | June 18 | July 18 | Aug. 18 | |

|---|---|---|---|---|---|

| Composite indicator | 100 | 108 | 108 | 109 | 108 |

| Past activity | –4 | 5 | 2 | 10 | 5 |

| Expected activity | –6 | 12 | 12 | 6 | 3 |

| Gen. business outlook | –17 | 10 | |||

| Past employment | –5 | 8 | 4 | 4 | 2 |

| Expected employment | –4 | 9 | 9 | 16 | 14 |

| Opinion on order books | –24 | –14 | –9 | –8 | –8 |

| Order books (in month) | 5.6 | 7.3 | 7.3 | 7.3 | 7.4 |

| Production capacity utilisation rate | 88.5 | 89.8 | 90.2 | 90.0 | 90.2 |

| Obstacles to production increase (in %) | 32 | 35 | 37 | 36 | 38 |

| - Because of workforce shortage (in %) | 13.7 | 14.9 | 16.3 | 15.3 | 17.0 |

| Recruiting problems (in %) | 57 | 72 | |||

| Expected prices | –14 | 5 | 4 | 8 | 4 |

| Cash-flow position | –10 | –17 | |||

| Repayment period | 30 | 34 |

- * Mean since April 1975 for the composite indicator and since

- September 1993 for the balances of opinion.

- Source: INSEE, French business survey in the building industry

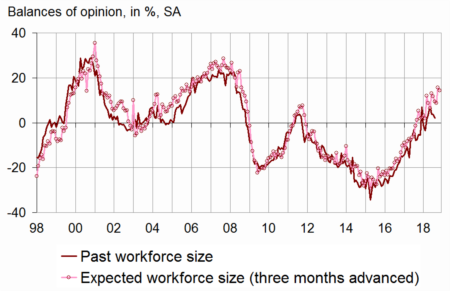

Fewer business managers report an increase in their past and expected staff size

In August 2018, fewer business managers than in July have reported an increase in their staff size over the last three months. Likewise, employment prospects are judged slightly less favourable: the corresponding balance of opinion has slipped back after a sharp rise in the previous month. Both balances on employment remain however well above their long-term average.

graphiqueGraph4 – Workforce size tendency in building construction

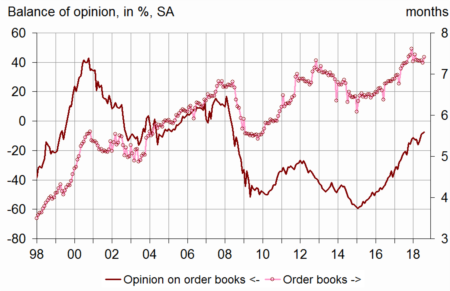

Order books remain judged well filled

In August 2018, as many business managers as in the previous month consider that their order books are well filled. The corresponding balance of opinion is stable, well above its long-term average. With their present staff size, business managers consider that their order books provide 7.4 months of work, a level close to that of last month and significantly higher than the long-term average (5.6 months).

graphiqueGraph5 – Order books

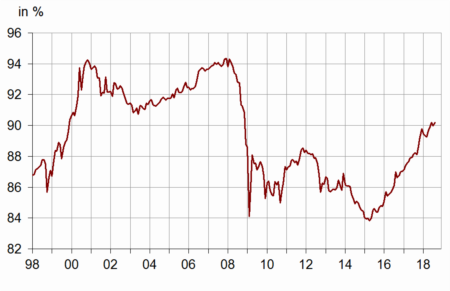

Higher capacity utilisation than on average

In August 2018, the production capacity utilisation rate has increased slightly after a small dip in the previous month. At 90.2%, it has returned to its June level, the highest since December 2008. This rate has stood above its long-term average (88.5%) since October 2017. At the same time, 38% of business managers have reported production bottlenecks, more than in the previous month and on long-term average. In particular, the proportion of business managers who have reported production bottlenecks because of workforce shortage has increased again. It has reached 17.0%, its highest level since November 2008, well above its long-term average (13.7%).

graphiqueGraph6 – Production capacity utilisation rate

Prices less often expected to rise

In August 2018, fewer business managers than in July have indicated that they will increase their prices over the next three months. The corresponding balance has fallen back but remains clearly above its long-term average.

Documentation

Abbreviated methodology (pdf,177 Ko)