4 May 2017

2017- n° 122In the manufacturing industry, business managers forecast a further increase in their

investment in 2017 Industrial investment survey - April 2017

4 May 2017

2017- n° 122In the manufacturing industry, business managers forecast a further increase in their

investment in 2017 Industrial investment survey - April 2017

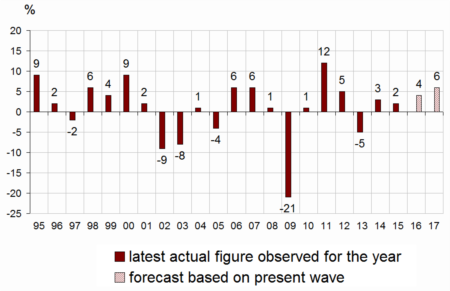

The business managers in industry surveyed in April 2017 stated that their investment increased by 4% in 2016 in nominal terms. For 2017, the business leaders in industry forecast a 6% increase in their investment spending compared with 2016.

The business managers in industry surveyed in April 2017 stated that their investment increased by 4% in 2016 in nominal terms. For 2017, the business leaders in industry forecast a 6% increase in their investment spending compared with 2016.

graphiqueGraph 1 – Annual nominal change in investment in the manufacturing industry

- Source: INSEE - Industrial investment survey

For 2017, business managers have revised upwards their investment forecast to 6%

Business managers in industry have upped by 1 point their January 2017 estimate whereas usually they maintain their forecast at that moment of the year (+0 point between 2005 and 2016). The upward revision is substential in the sector of electrical and electronic and machine equipment.

The estimate for 2017 might be revised during the next quarters: since 2004, the April forecast has overestimated by four points the actual investment growth finally observed in July the following year.

tableauTable 1 – Real annual investment growth in manufacturing industry by main sector

| NA* : (A17) et [A38] | In 2016 | In 2017 | ||

|---|---|---|---|---|

| estimate Jan.17 | estimate Apr.17 | forecast Jan.17 | forecast Apr.17 | |

| C : MANUFACTURING INDUSTRY | 4 | 4 | 5 | 6 |

| (C1): Manufacture of food products and beverages | 10 | 11 | 7 | 5 |

| (C3): Electrical and electronic equipment; machine equipment | 4 | 0 | 16 | 27 |

| (C4): Manufacture of transport equipment | 4 | 8 | –5 | –6 |

| [CL1]: Motor vehicles | 7 | 16 | –3 | –11 |

| (C5): Other manufacturing | 1 | 1 | 5 | 7 |

| Total sectors (C3-C4-C5) | 2 | 2 | 5 | 7 |

- How to read this table: In the manufacturing industry, firms surveyed in April 2017 observed a nominal investment increase of 4% in 2016 compared with 2015 and forecast an increase of 6% in 2017 compared with 2016.

- * The codes correspond to the level of aggregation (A17) and [A38] of the "NA" aggregate classification based on NAF rev.2.

- Source: INSEE - Industrial investment survey

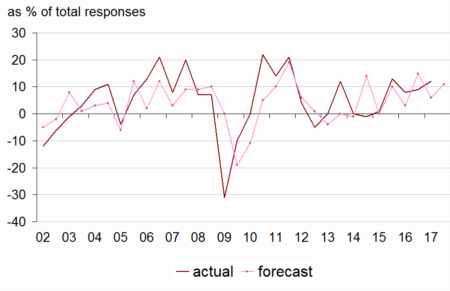

More business leaders forecast an increase than a decrease in their investment in H2 2017

In April 2017, more business managers in industry reported a rise rather than a fall in their investment for H1 2017. The corresponding balance (+12) is close to the October estimate, above its long-term average (+6).

For H2 2017, business managers remain optimistic: the corresponding balance has increased by 5 points compared with October (to +11) and remains above its long-term average (+6).

graphiqueGraph 2 – Opinion of industrials regarding six-month change in investment (first estimation)

- Source: INSEE - Industrial investment survey

Investment mainly aims at replacing the replacement and modernising of equipment

In 2017, the purposes of investment should be quite similar to those of 2016. The current distribution is close to the average distribution observed since 1991. The share of investment devoted to replacement stays the most important. A quarter of investment should be used for modernising equipment, the share for energy savings remains slightly above its long-term average. On the other hand, the share of investment aimed at increasing productive capacity or introducing new products is likely to remain a little below its long-term average.

tableauTable 2 – Breakdown of the purposes of investment

| Average | 2016 | 2017 | |

|---|---|---|---|

| 1991-2016 | actual | forecast | |

| Replacement | 27 | 28 | 27 |

| Modernization, streamlining | 24 | 23 | 24 |

| automation | 11 | 8 | 8 |

| new production methods | 7 | 6 | 8 |

| energy savings | 6 | 9 | 8 |

| Increase in productive capacity | 16 | 16 | 15 |

| Introduction of new products | 14 | 12 | 13 |

| Other purposes (safety, environment, working conditions…) | 20 | 21 | 21 |

- Source: INSEE - Industrial investment survey

The balance of opinion about the change in productive capacity observed in 2016 (+35) is higher than last year estimate (+28) and above its long-term average. For 2017, business leaders are more numerous than in 2016 to anticipate an increase in the productive capacity: the balance of opinion has reached +31 and equals its long-terme average.

tableauTable 3 – Productive capacity and equipment scrapping

| Observed | Forecast | ||||

|---|---|---|---|---|---|

| aver. | in 2016 | aver. | for 2016 | for 2017 | |

| Change in productive capacity* | 30 | 35 | 31 | 28 | 31 |

| Change in equipment scrapping* | 18 | 9 | –2 | –7 | –4 |

| Share of enterprises reporting equipment scrapping** | 75 | 66 | 74 | 67 | 66 |

| Breakdown of enterprises reporting equipment scrapping** | |||||

| Wear and tear, obsolescence | 52 | 54 | 49 | 49 | 56 |

| Installation of more efficient equipment | 31 | 29 | 33 | 29 | 32 |

| Shut-down of capacity for old products | 12 | 9 | 11 | 13 | 7 |

| Other scrapping | 5 | 8 | 6 | 9 | 5 |

- Source: INSEE - Industrial investment survey

Documentation

Methodology 2017 (pdf,147 Ko)

Pour en savoir plus

Time series : Industry – Investment