24 May 2016

2016- n° 133In May 2016, the business climate in services has returned to its long-term average Monthly survey of services - May 2016

24 May 2016

2016- n° 133In May 2016, the business climate in services has returned to its long-term average Monthly survey of services - May 2016

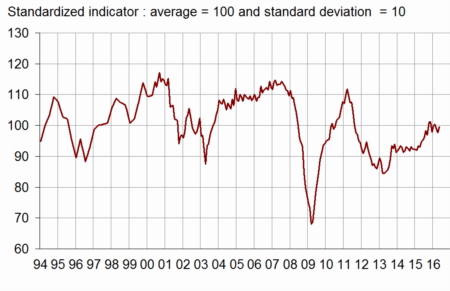

According to business managers surveyed in May 2016, the business climate in services has improved. The business climate composite indicator has recovered : increasing by two points, it has returned to its long-term average (100). The turning point indicator has moved back into the uncertainty area.

All services

According to business managers surveyed in May 2016, the business climate in services has improved. The business climate composite indicator has recovered : increasing by two points, it has returned to its long-term average (100). The turning point indicator has moved back into the uncertainty area.

graphiqueGraph1 – Business climate composite indicator

graphiquegraph_retourn – Turning point indicator

- Note: close to 1 (respectively −1), this indicator indicates a favourable short-term economic situation (respectively unfavourable). Between +0.3 and −0.3: uncertainty area.

The balance of opinion on the general outlook, which relates the assessment of business leaders over their whole sector, has increased slightly and has come back slightly above its long-term average.

The balance on past activity has fallen back slightly below its long-tem average. However, the balances on expected activity and demand have recovered; the balance on demand has returned just above its long-term average.

The balance on past employment is virtually stable whereas the balance on expected employment has improved markedly. Both balances remain well above their long-term average, particularly in temporary work agencies.

The balance on past investments has deteriorated and has fallen back to its long-term average. However, the balance on expected investments has recovered and has come back above its long-term average.

tableauTable_quarter – Economic outlook in the services sector

| Average* | Feb. 16 | March 16 | April 16 | May 16 | |

|---|---|---|---|---|---|

| Composite indicator | 100 | 100 | 99 | 98 | 100 |

| General outlook | –8 | –8 | –8 | –9 | –7 |

| Past activity | 2 | 0 | –1 | 3 | 1 |

| Expected activity | 2 | 0 | –1 | –3 | –1 |

| Expected demand | –1 | 1 | –2 | –5 | 0 |

| Past selling prices | –4 | –10 | –9 | –12 | –10 |

| Expected selling prices | –3 | –4 | –4 | –5 | –7 |

| Past employment | 3 | 7 | 11 | 13 | 12 |

| except temporary work agencies | 1 | 3 | 7 | 5 | 6 |

| Expected employment | 2 | 11 | 9 | 5 | 9 |

| except temporary work agencies | –1 | 2 | 0 | –4 | 1 |

| Investments | |||||

| Past investments | 1 | 6 | 6 | 7 | 1 |

| Expected investments | 1 | 3 | 3 | 0 | 4 |

- * Average of the balances of opinion since 1988

- Source: INSEE, business tendency survey in services

Road transport

In road freight, the balances on past and expected activity and employment have dipped slightly but they remain above their long-term average. The demand prospects have improved.

Accommodation and food services

In accommodation and food service activities, the balance on past activity is stable. The expectations on activity and demand have improved; the corresponding balances have come back above their long-term average. The balances on employment remain clearly above their long-term average.

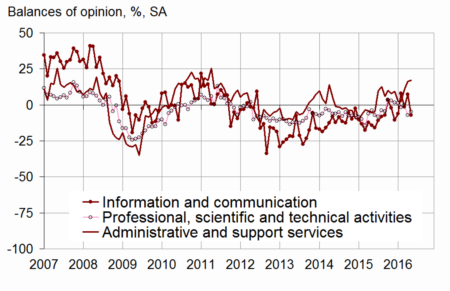

Information and communication

In information and communication, the balance on past activity has fallen anew and deviates further from its long-term average. Nevertheless, demand prospects have improved and the corresponding balance has come closer to its long-term average. The balances on employment remain close to their long-term average.

Real estate

In real estate, the balance on past activity has slipped back. The expactations on demand have deteriorated too. The corresponding balances deviate further from their long-term average. The balance on past employment has recovered whereas the balance on expected employment has decreased.

Professional, scientific and technical activities

In professional, scientific and technical activities, the balances on past and expected activity have edged up slightly. The balance on expected demand has increased markedly and has returned above its long-term average. The balance on expected employment has recovered, whereas the balance on past employment has gone down again and has come back below its long-term average.

Administrative and support service activities

In administrative and support service activities, the balances of opinion on activity and on past employment are virtually stable, clearly above their long-term average. Despite a decrease, the balance on expected employment remains high, particularly in temporary work agencies. The expectations on demand have improved also and the corresponding balance stands above its long-term average.

graphiquegraph_bonus_ – Past activity in services

tableauTable_det – Detailed data

| A21 | Average* | Feb. 16 | March 16 | April 16 | May 16 |

|---|---|---|---|---|---|

| (H) Road transport | |||||

| Past activity | –8 | –8 | –7 | –4 | –7 |

| Expected activity | –9 | –5 | –1 | –6 | –7 |

| Expected demand | –13 | –10 | –5 | –13 | –7 |

| Past employment | –8 | –5 | –6 | 3 | 0 |

| Expected employment | –10 | –3 | –2 | –2 | –7 |

| (I) Accommodation and food service activities | |||||

| Past activity | –7 | –5 | 3 | 2 | 2 |

| Expected activity | –7 | 0 | –10 | –17 | –5 |

| Expected demand | –9 | –7 | –12 | –13 | –4 |

| Past employment | –3 | –5 | 4 | 16 | 12 |

| Expected employment | –5 | 7 | 7 | 0 | 9 |

| (J) Information and communication | |||||

| Past activity | 8 | 8 | –1 | 7 | –7 |

| Expected activity | 10 | 2 | 1 | –3 | –4 |

| Expected demand | 10 | 11 | 10 | –1 | 7 |

| Past employment | 6 | 12 | 4 | 6 | 4 |

| Expected employment | 10 | 7 | 5 | 8 | 9 |

| (L) Real estate activities | |||||

| Past activity | 7 | –4 | –11 | 6 | –1 |

| Expected activity | 7 | 3 | –2 | 2 | 8 |

| Expected demand | 1 | –1 | –10 | –2 | –9 |

| Past employment | 3 | 1 | 9 | 0 | 5 |

| Expected employment | 2 | 4 | 0 | 3 | –1 |

| (M) Professional, scientific and technical activities | |||||

| Past activity | –1 | –2 | 0 | –7 | –5 |

| Expected activity | –2 | –4 | –4 | –5 | –3 |

| Expected demand | –6 | –6 | –6 | –11 | –5 |

| Past employment | 1 | 4 | 8 | 0 | –4 |

| Expected employment | 0 | 2 | 0 | –2 | 2 |

| (N) Administrative and support service activities | |||||

| Past activity | 6 | 2 | 11 | 16 | 17 |

| Expected activity | 5 | 8 | 10 | 9 | 8 |

| Expected demand | 3 | 9 | 5 | 4 | 8 |

| Past employment | 9 | 18 | 21 | 28 | 29 |

| Expected employment | 7 | 25 | 21 | 21 | 16 |

- * Average of the balances of opinion since 1988 (2006 for road transport)

Documentation

Methodology (2016) (pdf,158 Ko)

Pour en savoir plus

Time series : Economic outlook surveys – Services